In UAE lending, the bank statement is usually the most useful document in the application file. A salary certificate says what the applicant is supposed to earn. The statement shows what actually happened: salary credits, debt payments, returned items, cash deposits, transfers, balance volatility, and whether the story in the rest of the file is true.

That is why experienced credit teams read statements before they trust any other income document. The goal is not to find a single suspicious transaction. The goal is to understand whether the applicant's income, obligations, and cash behavior support the loan being requested.

Key Takeaways

- A UAE bank statement review should confirm salary credits, recurring obligations, account continuity, balance behavior, and document integrity.

- WPS salary credits are a strong signal for many private-sector employees, but they still need to match the applicant, employer, amount, and timing in the file.

- CBUAE Regulation No. 29/2011 caps installments for loans and facilities at 50% of the borrower's gross salary and regular income from a defined source.

- Red flags rarely stand alone. A cash deposit, crypto transfer, or missing page matters most when it changes affordability or contradicts other evidence.

- Automated bank statement analysis should triage risk and produce a structured audit trail, not replace every human lending decision.

What Lending Teams Need From a Bank Statement

A useful statement review answers five questions.

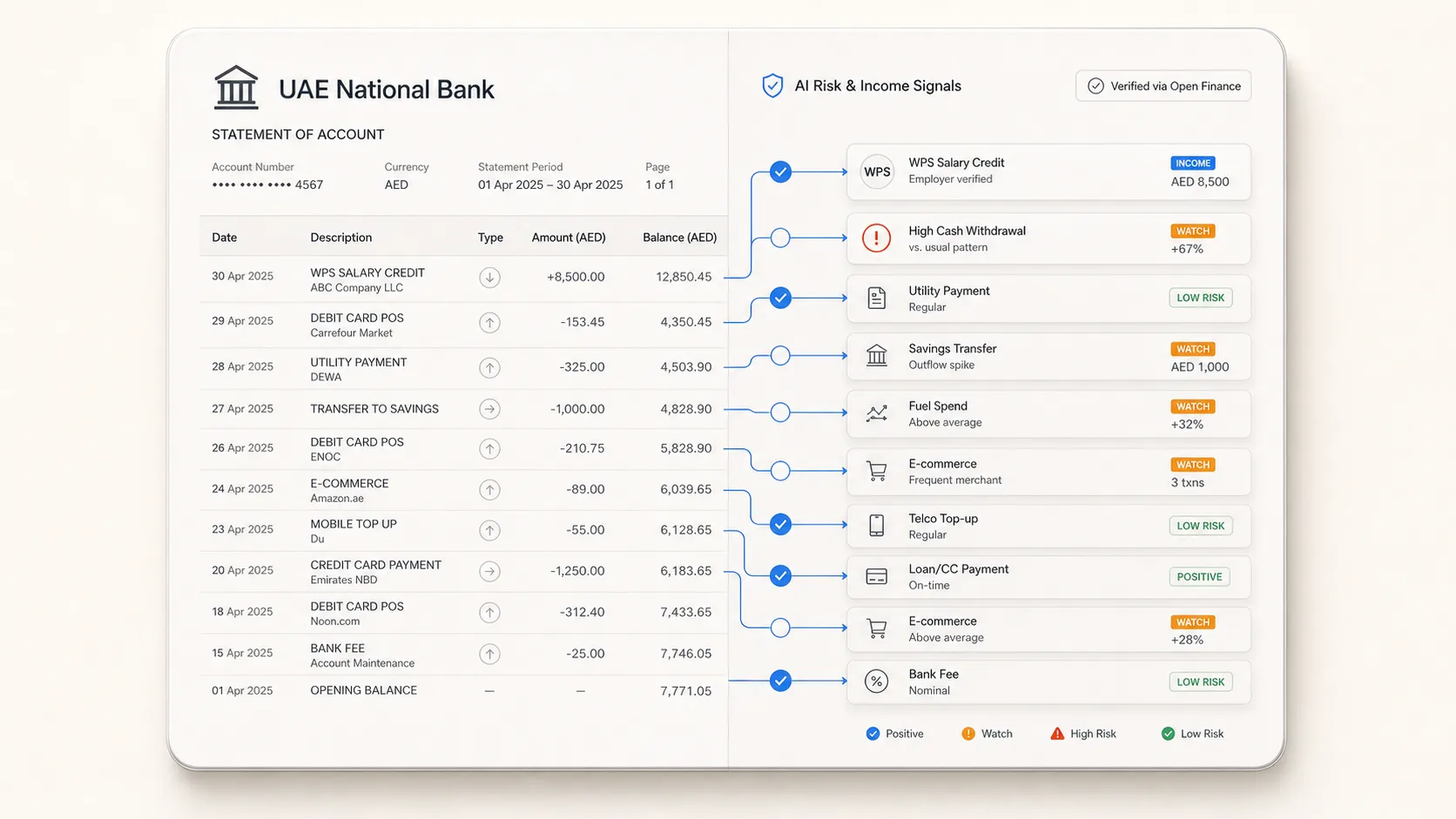

First, does the applicant receive income regularly? For salaried applicants, the reviewer looks for a salary credit, a WPS reference, or a repeating transfer from the employer. MoHRE says UAE labour market legislation requires private-sector establishments to pay workers monthly through the Wage Protection System, which transfers wages through approved banks, financial institutions, and exchange houses.

Second, does the income match the rest of the file? Salary certificate, Emirates ID, employer name, bank account holder, IBAN, visa status, and statement transactions should tell one coherent story. A mismatch does not always mean fraud, but it does mean the case needs explanation.

Third, what obligations already leave the account? CBUAE's Regulation No. 29/2011 says installments deducted by a bank or finance company for loans and facilities should not exceed 50% of the borrower's gross salary and regular income from a defined source. For a lending team, that makes recurring debits, card payments, auto finance, personal loan EMIs, BNPL-style payments, and standing instructions central to the review.

Fourth, is the statement complete and internally consistent? Opening and closing balances should reconcile. Page numbers should be continuous. The date range should cover the requested period. Missing months, cropped pages, or altered transaction rows turn a statement into a document-integrity problem.

Fifth, does the cash behavior support repayment? A borrower can have real income and still be risky because the account is constantly overdrawn, balance is inflated before application, or obligations consume most of the salary cycle.

The Red Flags That Matter Most

The strongest red flags are the ones that change the affordability picture or show that the statement may have been edited.

Salary credit does not match WPS or the salary certificate

If the salary certificate says AED 18,000 but the statement shows AED 12,000, the reviewer needs a reason. The applicant may receive allowances outside payroll, a commission may be seasonal, or the certificate may include benefits that are not cash salary. But the statement cannot be ignored. The repayment capacity comes from cash received, not from a number on letterhead.

Employer name or salary timing is inconsistent

Salary normally has a pattern: employer, amount range, frequency, and payment date. A one-off transfer from an unrelated company, a salary that arrives from a personal account, or deposits that change source every month may be valid for some workers, but they need classification before the loan decision.

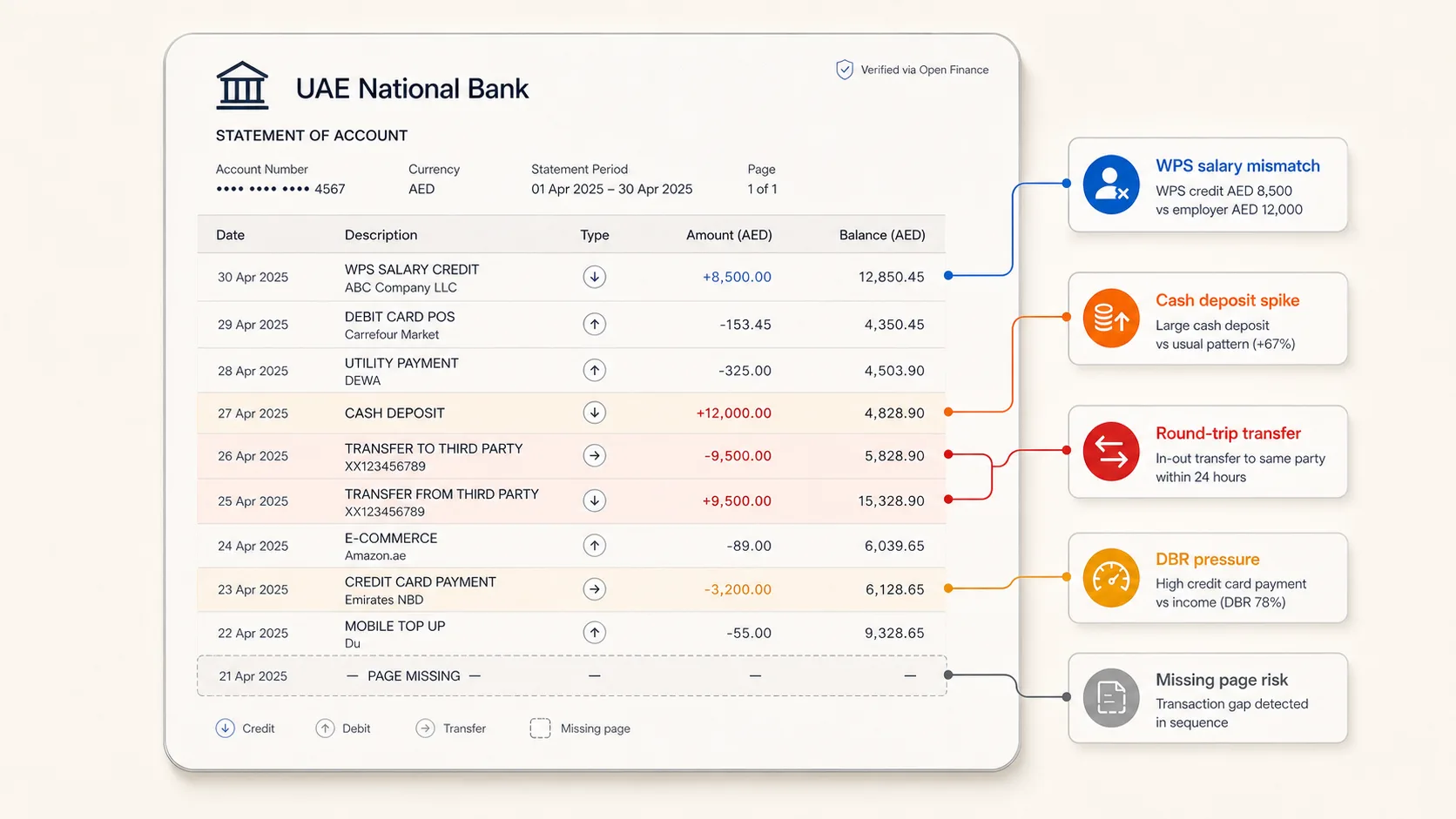

Large cash deposits before application

Balance inflation is common: the applicant deposits cash or receives a temporary transfer shortly before applying. The recent balance looks healthy, but the three- or six-month pattern says something else. Reviewers should compare recent balance against average balance, not just ending balance.

Round-trip transfers

Money leaves the account and returns from the same or connected parties shortly after. Sometimes the amounts are identical. Sometimes they are split to look natural. This can simulate activity, hide pass-through funds, or make income look stronger than it is.

Existing debt payments are understated

Some obligations are obvious: EMI, loan, finance, card auto-debit. Others are just recurring transfers to a finance company or another bank. If these are not classified, debt burden is understated and the loan may appear affordable when it is not.

Bounced cheques, failed direct debits, and return items

The UAE changed bounced-cheque enforcement in 2022, and insufficient-funds cheques are no longer automatically the same criminal process they once were. That legal change does not make returned payments irrelevant for credit risk. A bounced cheque or failed debit still shows a liquidity failure at the time the payment was due.

Gambling or high-risk merchant activity

Recurring betting, casino, or high-risk gaming merchant activity matters because it signals volatile outflows. The issue for lenders is repayment risk and explainability. Categorization should look beyond obvious merchant names because many transactions appear through payment processors or wallets.

Crypto exchange transfers

Crypto activity is not automatically a rejection reason. Dubai has a formal virtual-asset framework through VARA, and licensed virtual-asset service providers can operate in or from Dubai under VARA rules. For a lender, the risk question is narrower: are recurring transfers to exchanges reducing disposable income, adding volatility, or making source-of-funds analysis harder?

Business and personal funds are mixed

A personal account that receives supplier payments, customer refunds, platform payouts, and personal salary is difficult to underwrite. The applicant may be solvent, but the lender has to separate income from business turnover and pass-through money.

Missing pages, cropped periods, or broken balance continuity

Missing pages are not a formatting issue. They prevent the reviewer from confirming whether the statement is complete. A six-month statement that skips one month, starts mid-period, or has non-matching balances should be treated as incomplete until the original file is provided.

How CBUAE Debt Burden Rules Affect Review

Debt burden is not a generic risk metric in the UAE. CBUAE Regulation No. 29/2011 states that installments for loans and facilities should not exceed 50% of the borrower's gross salary and regular income from a defined source. CBUAE mortgage clarifications also reference that same 50% maximum debt-burden limit.

For statement review, the practical implication is simple: the statement has to identify recurring obligations accurately enough to support the calculation.

| Statement signal | Why it matters for DBR or affordability |

|---|---|

| Salary credit amount and frequency | Establishes the income side of the calculation. |

| Loan EMI or finance debit | Counts toward recurring debt obligations. |

| Credit card auto-payment | Shows card repayment burden and possible revolving debt. |

| BNPL or short-term instalments | May not look like a loan unless categorized correctly. |

| Standing instruction to another bank | Can hide an obligation if the beneficiary is not recognized. |

| Returned payment or overdraft fee | Shows liquidity stress even if formal DBR appears acceptable. |

The mistake is to calculate affordability from the salary certificate alone. A statement can reveal obligations that are not visible in the certificate, and it can show that salary does not stay in the account long enough to support the proposed repayment.

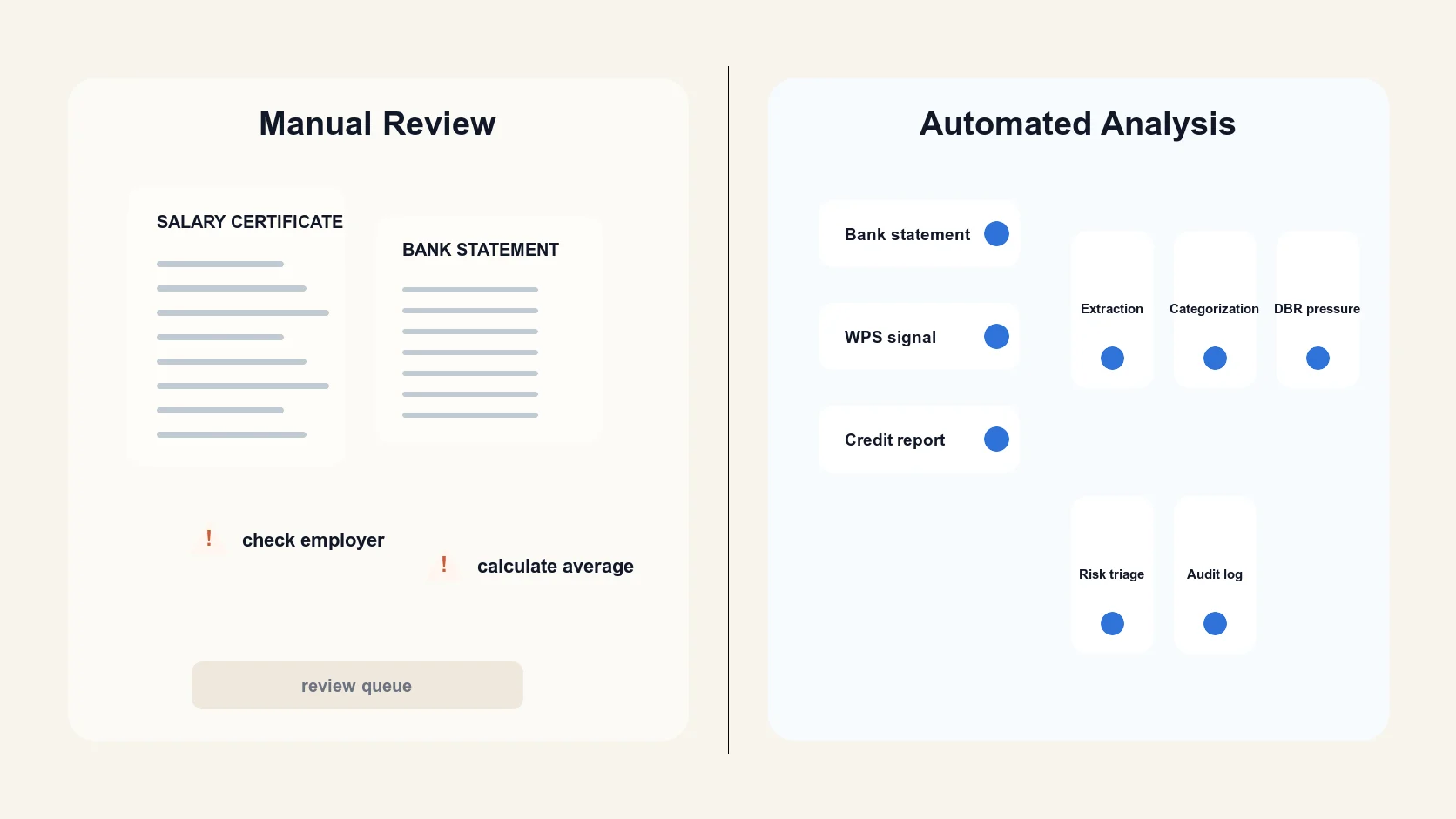

Where Manual Review Fails

Manual review is good at judgment but weak at repetition. A trained reviewer can see that a statement feels wrong. The problem is applying that judgment consistently across thousands of pages, many banks, many layouts, and many transaction descriptions.

There are four common failure modes.

First, reviewers miss low-frequency patterns. A round-trip transfer may involve transactions ten days apart. A salary mismatch may only appear when comparing three months of bank statement history with the salary certificate. Humans are not built to memorize every row across every page.

Second, transaction labels vary. The same obligation can appear as EMI, installment, finance, repayment, standing order, or a company name. Without a categorization model, the reviewer may not count it consistently.

Third, document manipulation can look clean. A bank statement PDF can have edited rows, missing pages, altered balances, or rebuilt table sections. Visual review alone does not check metadata, font consistency, layout structure, or pixel-level anomalies.

Fourth, the audit trail is thin. A manual note saying "statement reviewed" does not explain which rows were counted, which obligations were excluded, or why a red flag was overridden.

How Automated Bank Statement Analysis Works

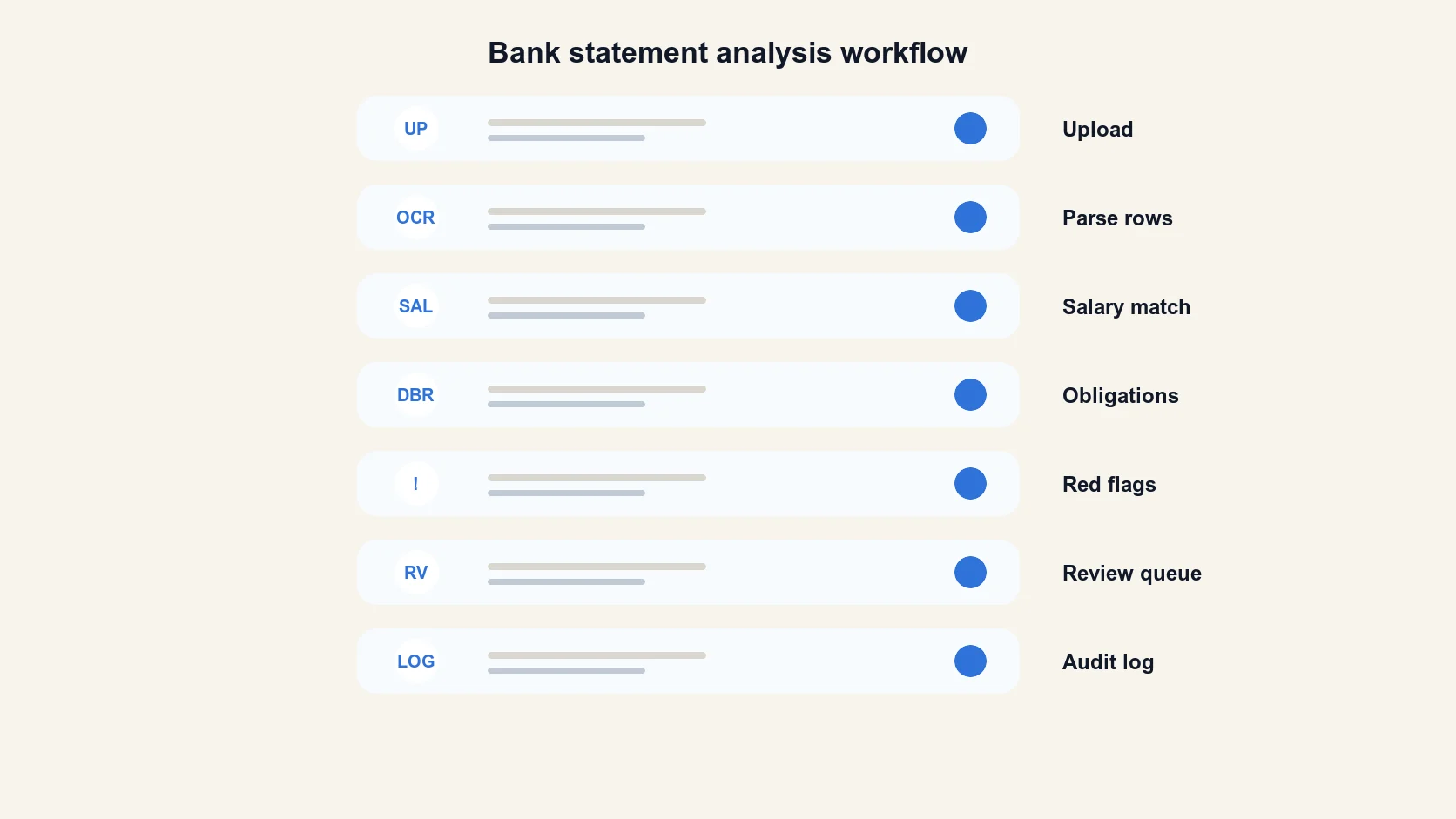

Automation should not turn lending into a black box. It should turn a bank statement into a structured review package.

The workflow starts with file intake. The system checks whether the statement is complete, readable, and internally consistent. It extracts account holder, IBAN, statement period, opening and closing balances, transaction rows, page count, and bank format.

Next comes transaction classification. Salary credits, loan payments, card repayments, cash deposits, transfers, bounced items, fees, crypto exchange transfers, gambling merchants, rent, school fees, remittances, and business turnover all need different labels.

Then the system calculates signals: verified income, income volatility, average balance, minimum balance, cash buffer, recurring obligations, debt burden pressure, round-trip transfers, suspicious deposits, and missing-period risk.

Document-integrity checks run alongside the financial analysis. Metadata, layout, font consistency, and pixel-level indicators help decide whether the statement can be trusted.

The output should be a review package: extracted rows, categories, risk flags, reason codes, confidence scores, and a structured audit trail. A human reviewer can still make the final decision, but the work starts from evidence rather than raw pages.

What to Route for Human Review

Not every flag should block an application. Some should route the case to a reviewer with context.

Route the case when income is real but variable, because the question becomes sustainable repayment. Route it when the salary certificate and statement disagree, because the reviewer needs to decide whether allowances, commission, or employer timing explains the gap. Route it when a document-integrity signal appears, because a manipulated PDF should not be treated like a clean bank statement.

Route it when the statement mixes personal and business activity. Automated analysis can separate categories, but a human may need additional documents before using the account as proof of income. Route it when obligations are high but not clearly loan-related. A recurring transfer to a person could be rent, family support, or repayment of an informal debt.

The design goal is a smaller, better review queue. Clean applications can move quickly. High-risk applications can be declined or escalated. Ambiguous applications land in front of a human with the relevant rows already highlighted.

Implementation Checklist

For a UAE lending team, a statement-review checklist should include:

- statement period, page count, and balance continuity;

- account holder and IBAN match against the applicant file;

- salary credits, WPS references, and employer consistency;

- recurring obligations and DBR-related payment categories;

- cash deposits, round-trip transfers, and unusual incoming funds;

- returned items, overdraft fees, and failed direct debits;

- high-risk merchant categories, including gambling and crypto exchange transfers;

- document-integrity checks for edited PDFs or missing pages;

- reason codes and audit logs for every automated flag;

- post-to-post links into KYC and document fraud review when the problem is not just financial.

For adjacent controls, read the KYC automation guide and the document fraud detection guide. For implementation, start with bank statement analysis and pair it with fraud detection.

FAQ

What is the biggest red flag in a UAE bank statement?

The most important red flag is usually an income mismatch: salary credits in the statement do not match the salary certificate, employer, timing, or WPS evidence. It directly affects affordability.

Does a cash deposit always mean the application should be rejected?

No. A cash deposit can be legitimate. It becomes a red flag when it appears shortly before application, changes the apparent balance, and is not supported by a clear source.

How does DBR affect bank statement review in the UAE?

The CBUAE 50% installment limit means reviewers need to identify existing recurring obligations accurately. A bank statement is one of the main places those obligations appear.

Are crypto transactions an automatic rejection reason?

No. Crypto transfers should be assessed as part of disposable-income, volatility, and source-of-funds review. The UAE has regulated virtual-asset activity, but a lender still needs to understand the repayment impact.

Can automated analysis replace a credit officer?

No. Automation extracts rows, categorizes transactions, detects patterns, and routes risk. The credit officer still owns judgment, policy exceptions, and final accountability.

What documents should be checked alongside the bank statement?

Salary certificate, Emirates ID, employer evidence, credit report, WPS salary records where available, and any supporting document needed to explain business income or unusual transfers.

Sources

If you want to learn more, you can try the demo or read our tool documentation.