Document fraud in UAE financial services is rarely a completely invented identity. More often, it is a real applicant with one manipulated document: a salary certificate with a changed amount, a bank statement with rows removed, a trade license with an altered date, or a passport copy paired with inconsistent supporting evidence.

That is why document fraud detection cannot be one visual check. The system has to inspect the file, the pixels, the typography, the layout, the issuing context, the signature, and the relationship between documents in the application.

Key Takeaways

- Metadata, fonts, pixels, layout, signatures, and content consistency each catch a different fraud pattern.

- PDF metadata is useful but not conclusive. Adobe's PDF documentation notes that PDFs can include author, creation date, modification date, and XMP metadata, but metadata can be missing or changed.

- UAE-specific checks matter because documents can be bilingual, issued by different authorities, digitally signed, or verifiable through UAE Verify or UAE PASS.

- Pixel-level analysis is a signal, not proof. Digital forensics requires multiple artifacts and human-review escalation for ambiguous cases.

- Automated fraud detection should return evidence, confidence, and reason codes, not just a pass/fail result.

What Document Fraud Looks Like in Practice

Most forged documents start from something real. A genuine salary certificate becomes a higher salary. A legitimate bank statement has transactions removed. A trade license is copied from a real business and edited. A digitally printed PDF is rebuilt in a design tool, then exported again.

Common UAE financial-services cases include:

- salary certificates with inflated salary, changed joining date, or fake allowance lines;

- bank statements with deleted debt payments, inserted salary credits, or altered closing balances;

- Emirates ID copies paired with inconsistent names, dates, or supporting documents;

- passport and visa pages where expiry dates or employer information do not match the file;

- trade licenses with changed activity, expiry, establishment name, or license number;

- employment letters that look plausible but cannot be reconciled with salary credits.

These edits can pass a quick visual check because the document still looks professional. Detection starts when the system asks whether the file behaves like a genuine original from that source.

The Signals Each Detection Method Checks

No single method catches every forgery. Good systems combine weak signals into a stronger case.

Metadata analysis

PDFs can carry metadata such as author, creator tool, producer, creation date, modification date, and XMP fields. If a salary certificate dated January was created yesterday in an online editor, the file deserves review. If a bank statement's producer does not match the expected bank export path, that is useful context.

Metadata cannot prove authenticity by itself. Some legitimate systems strip metadata. Some forgers remove or rewrite it. PDF Association guidance also warns that some PDFs contain no useful metadata at all. Treat metadata as one signal.

Layout and template analysis

Official and bank-issued documents follow repeatable structures: margins, table widths, logo positions, QR locations, date fields, page numbering, and footer language. A manipulated document often breaks those relationships. A new salary amount may push alignment off-grid. A removed transaction row may leave spacing that does not match the rest of the table.

Template analysis is strongest when the system has a reference set for the issuing bank, employer, government entity, or free-zone authority.

Font and typography analysis

Edited text often uses a different font, weight, kerning, baseline, or rendering engine from the original. A forged salary number may visually look close, but the digit spacing may not match the rest of the line. Arabic and English text can have different typography rules, so UAE documents need checks for both scripts.

Font analysis is not perfect. A forged document rebuilt from a template can be consistent. A legitimate document generated by a new system version may also differ from older samples. That is why typography should be combined with source, layout, and content checks.

Pixel-level analysis

Image-based documents carry compression and editing artifacts. If a scanned bank statement has one transaction row with different compression behavior, sharpness, or noise, that region may have been pasted or regenerated.

Pixel analysis is especially useful for scanned PDFs, phone photos, stamps, and signatures. It is less useful for clean native PDFs with selectable text. It should also be treated carefully: NIST's review of digital investigation techniques notes that forensic interpretation depends on software versions, artifacts, and limitations. A pixel anomaly is a reason to investigate, not a courtroom verdict.

Digital signature and verification checks

Digitally signed documents give a stronger signal. UAE PASS supports signing and verifying documents digitally. UAE Verify says it can validate Digital Trusted Documents by checking authenticity, integrity, validity, and official source.

If a document is supposed to be digitally verifiable, the workflow should check the signature or verification channel before relying on the PDF. If a signed document was modified after signing, the signature should not validate.

Content consistency checks

Some fraud is visible only across documents. A bank statement salary credit may not match the salary certificate. An Emirates ID name may not match the account holder. A visa employer may not match the employer letter. A trade license activity may not match the claimed business revenue.

Cross-document consistency is often the best fraud signal because it asks whether the whole file tells one story.

| Method | What it catches | What it misses |

|---|---|---|

| Metadata | Recent edits, unusual creator tools, missing provenance | Clean recreations and stripped metadata |

| Layout | Moved fields, broken tables, template mismatch | New legitimate templates without reference samples |

| Fonts | Re-typed numbers, pasted fields, inconsistent rendering | Full-template rebuilds with matching fonts |

| Pixels | Pasted regions, altered scans, copied stamps | Native PDFs and low-quality originals |

| Signatures | Modified signed documents and unverifiable originals | Documents that were never signed |

| Cross-checks | Inconsistent income, identity, employer, or license data | Fraud where every document was forged consistently |

Why UAE Documents Need Local Context

UAE document review has local complexity that generic fraud tools miss.

Many documents are bilingual. Arabic text is right-to-left, glyphs join differently depending on position, and fields may appear in both Arabic and English. A system trained only on Latin text can miss inconsistencies in the Arabic half of a document.

Issuing authorities vary. Trade licenses can come from mainland departments, free zones, ADGM, DIFC-related entities, DMCC, JAFZA, DAFZA, and others. Bank statement formats vary by bank, account type, and export channel. Salary evidence may come from a company letter, WPS salary credits, or bank statement history.

Digital verification is also more common than many reviewers assume. UAE Verify and UAE PASS make some official digital documents verifiable without relying only on the visual PDF. If a document carries a QR code or digital signature, the workflow should try to verify it instead of treating it like a scan.

Finally, document quality varies. Some applicants upload original PDFs. Others upload phone photos of printed copies. A poor scan is not fraud by itself, but it reduces confidence and may require fallback checks.

Where False Positives Come From

False positives are expensive because they slow good applicants and overload compliance teams.

A legitimate statement may have no metadata because the bank export stripped it. A salary certificate may be created in Word because the employer's HR system is basic. A scanned document may show pixel artifacts because it was photographed in bad lighting. A free-zone trade license may use a template the model has not seen before.

The answer is not to ignore these signals. The answer is to score them correctly.

Low-confidence fraud signals should route to review, not automatically reject. Stronger combinations should escalate faster: edited metadata plus font mismatch plus salary inconsistency is more serious than any one of those signals alone.

Good fraud detection separates three outcomes:

- clean enough to proceed;

- suspicious enough for human review;

- high-risk enough to decline or request an original verifiable document.

Manual Review vs Automated Detection

Manual review is still needed for judgment. It is weak at repetitive forensic inspection.

| Review task | Manual review | Automated fraud detection |

|---|---|---|

| Metadata inspection | Often skipped unless the reviewer opens file properties. | Extracts creator, producer, dates, XMP, and file history signals. |

| Font and layout consistency | Visual judgment, hard to apply across pages. | Compares line spacing, glyph behavior, table structure, and templates. |

| Pixel anomalies | Usually invisible at normal zoom. | Highlights suspicious regions and compression differences. |

| Signature verification | Depends on reviewer knowing where to check. | Tests digital signatures and verification channels when present. |

| Cross-document checks | Manual comparison across files. | Links names, IDs, employers, salary amounts, account holders, and dates. |

| Audit trail | Notes and screenshots. | Structured evidence, reason codes, confidence, and reviewer overrides. |

The important design choice is explainability. A fraud system should show why it flagged a document. "High risk" is not enough. The reviewer needs to see that the salary field has a font mismatch, the PDF was modified after issue date, the salary credit does not match, and the bank statement page count is incomplete.

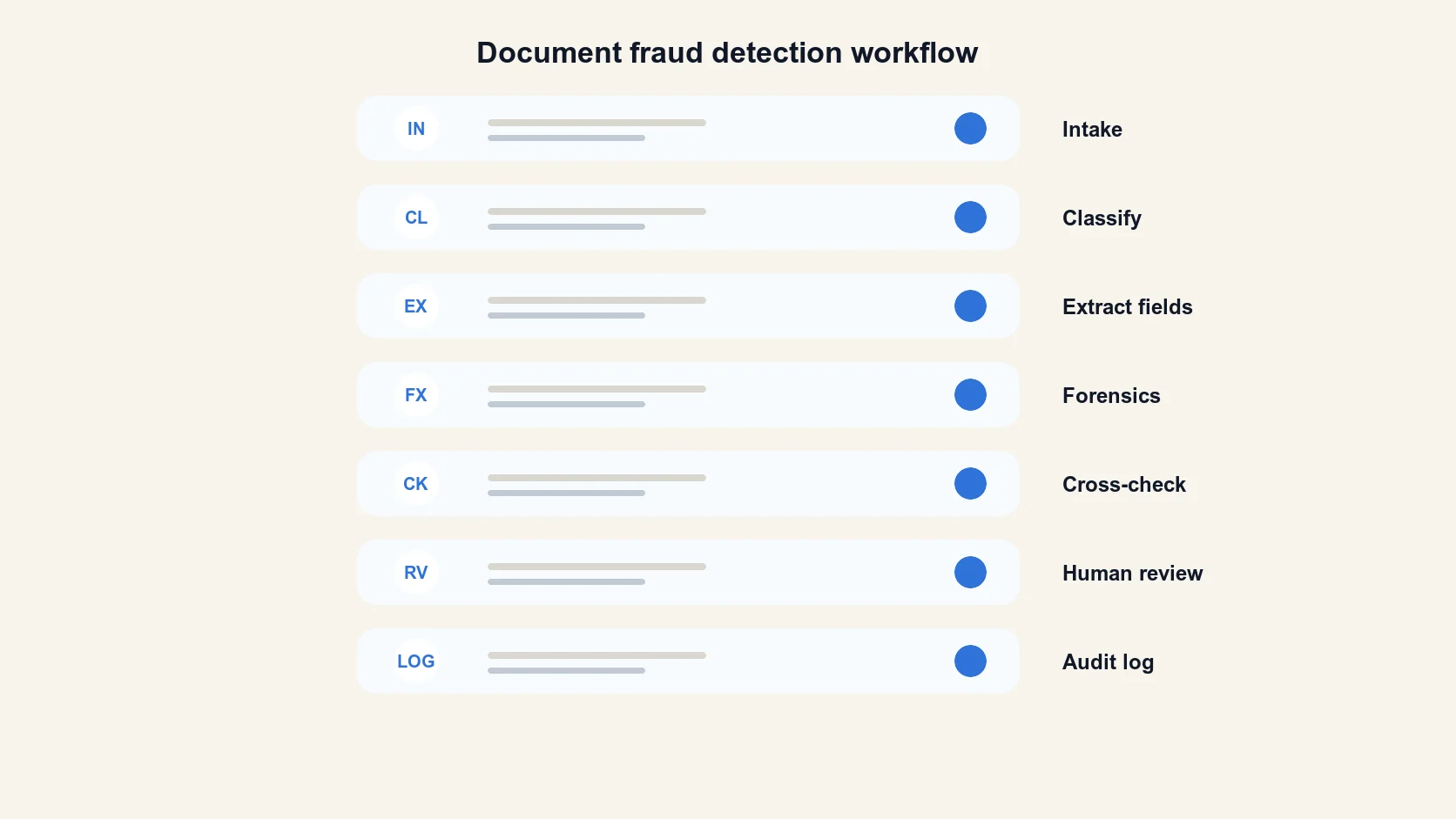

How Automated Document Fraud Detection Works

An automated fraud workflow starts with intake. It identifies document type, file type, page count, language, source clues, and whether the file is native PDF, scan, image, or mixed.

Then it extracts fields: name, ID number, employer, salary, dates, account holder, IBAN, trade license number, expiry, and issuing authority. Extraction gives the system data to compare across documents.

Next, forensic checks run in parallel. Metadata analysis checks provenance. Layout analysis checks structure. Font analysis checks typographic consistency. Pixel analysis checks altered regions. Signature checks validate signed or digitally verifiable documents when possible.

After that, the system compares documents to each other. Does the bank statement account holder match the applicant? Does the salary credit match the salary certificate? Does the trade license name match the business statement? Does the employer name appear consistently across visa, salary letter, and bank credits?

Finally, the workflow produces a review package: document type, extracted fields, fraud signals, confidence score, highlighted regions, source checks, and recommended action.

What to Route for Human Review

Route cases where the document may be legitimate but confidence is low. A poor scan, an unfamiliar template, or missing metadata should not automatically reject a borrower. It should ask for better evidence or a reviewer decision.

Route cases where one signal is strong but context is unclear. A modification date after the document date may be explainable if HR reissued the certificate. A font mismatch may be harmless if the document was generated by a new template. The reviewer needs supporting evidence.

Route cases where multiple signals agree. Metadata edit, font mismatch, salary inconsistency, and missing WPS salary credit together are much stronger than any single flag.

The best review queue is small and evidence-rich. The reviewer should not search through five PDFs from scratch. They should open the case and see the suspicious field, the supporting rows, and the recommended next step.

Implementation Checklist

For a UAE document-fraud workflow, start with these controls:

- classify document type before applying fraud rules;

- extract key fields and compare them across the application;

- check metadata, creator, producer, dates, and XMP where available;

- compare layout and typography against known templates;

- run pixel-level checks on scans, images, stamps, and signatures;

- validate UAE PASS, UAE Verify, QR, or digital signature channels where present;

- treat poor quality as low confidence, not automatic fraud;

- route ambiguous cases to human review with evidence;

- store every signal, override, and final decision in an audit log;

- connect document fraud checks to KYC automation and bank statement red flags.

For implementation, pair fraud detection with bank statement analysis, Emirates ID verification, and passport scanning where identity and income evidence meet.

FAQ

Can PDF metadata prove a document is fake?

No. Metadata can show useful inconsistencies, but it can be missing, stripped, or changed. It should be treated as one signal in a broader fraud score.

Does pixel analysis work on all PDFs?

No. Pixel-level checks work best on image-based documents, scans, photos, stamps, and signatures. Native PDFs with selectable text need metadata, font, layout, and structure checks as well.

Are digitally signed UAE documents safer?

Yes, if the signature or verification channel validates. UAE PASS and UAE Verify can make some official digital documents easier to authenticate, but the workflow still needs to confirm the document belongs to the applicant and matches the rest of the file.

Why do legitimate documents get flagged?

Poor scans, new templates, stripped metadata, bilingual layouts, and low-quality uploads can all trigger suspicion. That is why low-confidence cases should route to review instead of being rejected automatically.

What documents are most often checked for fraud in lending?

Salary certificates, bank statements, Emirates ID copies, passport and visa pages, trade licenses, employment letters, and proof-of-address documents.

Does automation replace the fraud analyst?

No. Automation finds patterns, extracts evidence, and prioritizes cases. Analysts still decide ambiguous cases, tune policy, and own final accountability.

Sources

If you want to learn more, you can try the demo or read our tool documentation.