UAE BNPL is no longer just a checkout feature. Under the Central Bank of the UAE's short-term credit framework, it is a regulated credit workflow that needs verified income, affordability checks, credit reporting, fraud controls, and an audit trail.

That changes the operating model. A salary certificate attached to an application is not enough. A reviewer still has to confirm income, identify existing debt obligations, calculate whether the credit limit is affordable, and document why the application was approved or rejected.

Key Takeaways

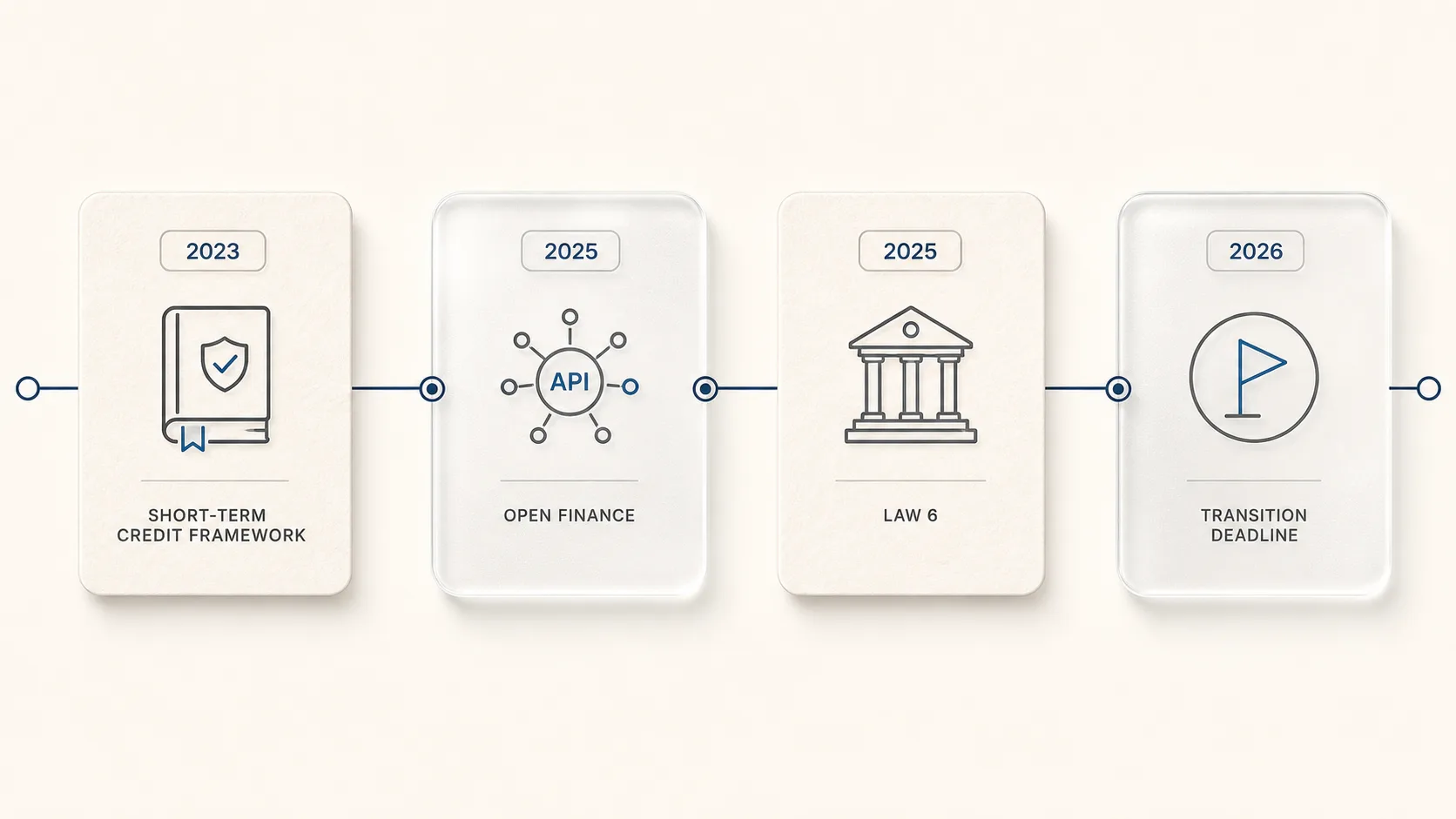

- CBUAE's Finance Companies Regulation, Circular No. 3/2023, treats short-term credit as a regulated activity and caps a borrower's total short-term credit at the lower of AED 20,000 or three months of verified net income.

- The same framework requires affordability assessment, credit-reporting controls, and a documented credit file. Income verification is not just an onboarding preference.

- UAE open finance is moving the market toward consent-based, API-delivered account data, but bank statement analysis and WPS salary evidence still matter as coverage and adoption mature.

- The old AED 5,000 personal-loan salary floor was reported removed in late 2025, but banks can still apply their own risk criteria. That makes automated affordability checks more important, not less.

- The right stack is layered: bank statement analysis, WPS salary signals where available, credit bureau checks, document fraud detection, policy rules, human review, and audit logging.

What Changed in the CBUAE Rules

The core BNPL rule sits in the CBUAE Finance Companies Regulation, Circular No. 3/2023. The rulebook lists it as effective from 29 September 2023, while CBUAE's public short-term credit framework announcement followed on 27 December 2023. For operators, the important point is the same: BNPL-style short-term credit is inside the regulated finance-company perimeter.

Article 23 of the regulation sets the practical affordability boundary. A restricted licence finance company or agent cannot extend more than AED 20,000 in total short-term credit to a borrower, or more than three months of that borrower's verified net income, whichever is lower. The maximum repayment term is twelve months. The framework also requires affordability assessment and fair treatment of borrowers.

Article 24 adds credit-reporting and credit-file obligations. For short-term credit of AED 5,000 or more, the provider must request credit information before extending credit. The provider must also review borrower information, conduct an affordability assessment, verify the borrower's solvency and ability to repay, and document that verification in a credit file.

That is why income verification matters. The compliance question is not "did the applicant upload a salary certificate?" The question is "can the provider show how income, existing obligations, credit exposure, and document risk were assessed before credit was granted?"

The second change is the broader regulatory environment. Federal Decree-Law No. 6 of 2025 came into force on 16 September 2025. CBUAE's own legislation FAQ says entities and individuals have a one-year reconciliation period from that effective date, ending one year later. That makes 16 September 2026 the practical transition date to watch for newly captured or newly structured financial activities.

Open finance is the third change. The UAE's Open Finance Regulation, updated by Circular 3 of 2025 and in force from 10 July 2025, builds a framework for consent-based data sharing and service initiation. It uses a centralized API hub and common infrastructure, with Nebras operating the API hub and related services. For BNPL providers, this points toward direct, permissioned income and transaction data over time.

The salary-floor change is separate. Khaleej Times reported in December 2025 that CBUAE had removed the AED 5,000 minimum salary requirement for personal loans, while banks still maintained their own eligibility thresholds. Treat this as a market-access signal, not a free pass. Lower and more variable incomes make affordability verification harder, and the lending institution still owns the credit decision.

| Rule or market change | What it means for BNPL income verification |

|---|---|

| Short-term credit cap | The provider needs verified net income to apply the lower of AED 20,000 or three months' income. |

| AED 5,000 credit-report threshold | Applications at or above the threshold need credit information before credit is extended. |

| Affordability assessment | The provider needs a defensible view of income, obligations, and repayment ability. |

| Open Finance Regulation | Consent-based account data becomes the long-term direction for verified income and transaction data. |

| Removal of fixed salary floor | More applicants may enter the funnel, but banks and finance providers still apply risk-based eligibility. |

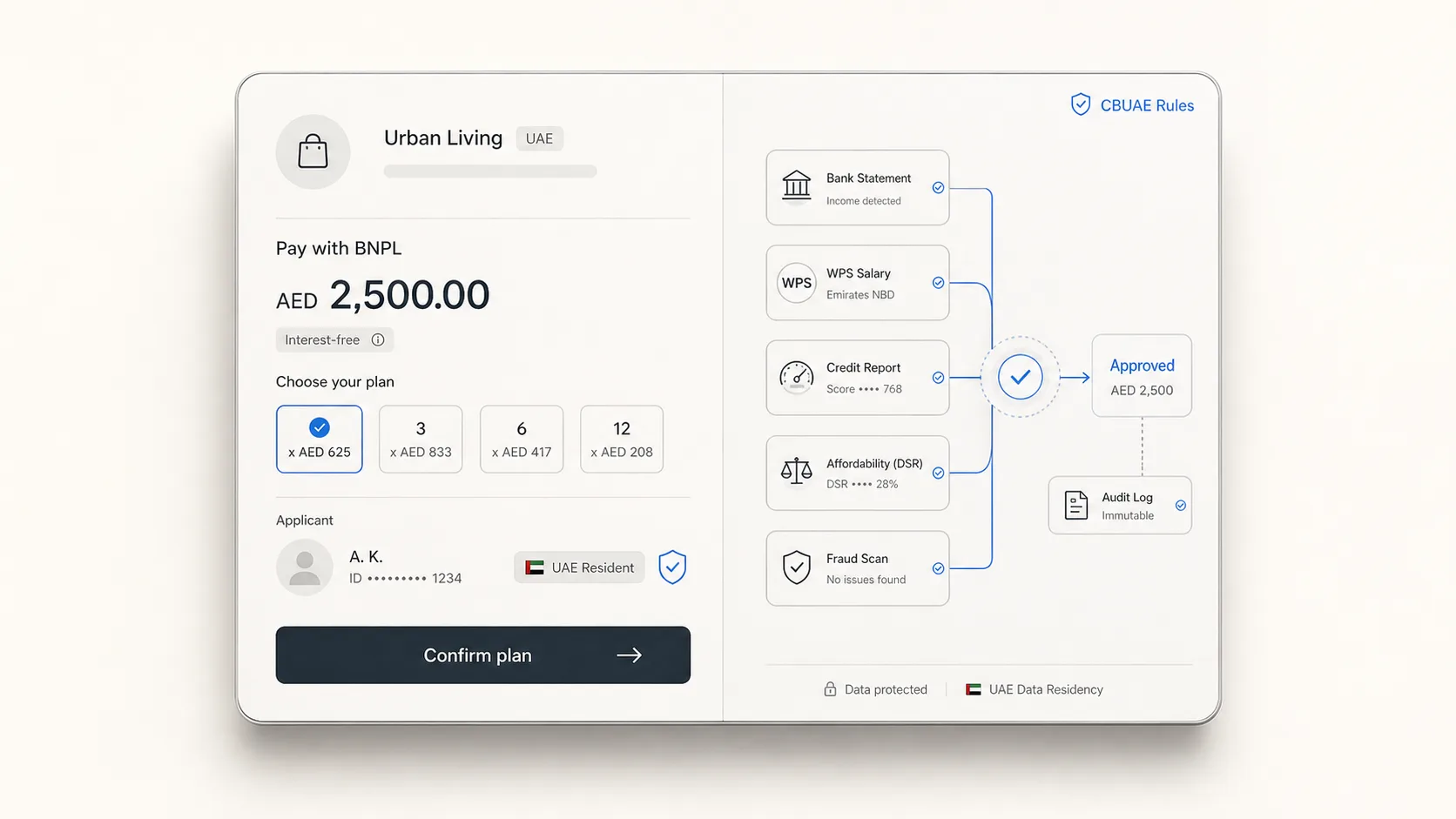

The Compliance Stack for BNPL Income Verification

A compliant BNPL verification workflow is not one check. It is a stack of evidence and controls.

The first layer is identity and applicant consistency. The provider needs to know that the applicant, Emirates ID, phone number, bank account, and submitted documents all belong to the same person. This is where KYC and income verification meet.

The second layer is income evidence. The strongest signal depends on the applicant. A salaried private-sector employee may have WPS salary credits. A free-zone worker may rely more heavily on bank statements. A gig worker or small business owner may have irregular inflows that need transaction-level classification rather than a single monthly salary field.

The third layer is existing obligations. For BNPL, the risk is often not one large loan. It is many small instalments across multiple providers, cards, and accounts. A salary certificate does not reveal that. Bank statements and credit reports do.

The fourth layer is document integrity. Salary certificates and bank statements are easy to edit. Metadata checks, font consistency, layout comparison, and pixel-level analysis help identify whether a submitted file has been manipulated before the income figure is trusted.

The fifth layer is policy logic. The system needs to apply the provider's rules consistently: maximum exposure, credit bureau trigger, affordability thresholds, manual review conditions, high-risk merchant categories, repeat-applicant behavior, and adverse document flags.

The final layer is auditability. Every input, extraction, rule result, override, and final decision should be stored with a timestamp. That is the difference between a decision and a defensible compliance record.

Why Manual Salary Certificates Break at Scale

Manual review works only while the applicant pool is small, clean, and repetitive. UAE BNPL is not moving in that direction. Research and Markets projected the UAE BNPL market to grow from USD 1.17 billion in 2025 to USD 1.47 billion in 2026, then to about USD 3.92 billion by 2031. More volume means more edge cases.

Manual verification has three structural failures.

First, reviewers cannot consistently read every document at speed. A single clean salary certificate might take minutes. A messy case requires employer-name validation, income cross-checks, bank statement review, recurring-obligation analysis, and escalation notes. At hundreds or thousands of applications per day, the queue becomes the product bottleneck.

Second, a salary certificate is a weak affordability source by itself. It says what someone is supposed to earn. It does not show whether salary arrives on time, whether the applicant already has loan instalments, whether the account is overdrawn between pay cycles, or whether a recent cash deposit inflated the balance before application.

Third, manual review creates inconsistent evidence. One reviewer writes a note. Another reviewer checks the credit report but does not record the reason. A third reviewer approves because the salary looks plausible. If a regulator, auditor, or risk manager asks why the provider granted credit, the answer is scattered across emails, PDFs, and case comments.

That is why automation matters even when the final decision stays human. Automation standardizes the first pass, highlights the exception, and records the basis for review.

The Documents and Data Sources That Matter

BNPL providers usually need more than one income source because UAE employment patterns vary.

Bank statements are the broadest source. They show salary credits, cash deposits, recurring obligations, bounced payments, transfers to other lenders, card repayments, balance volatility, and spending behavior. For bank statement analysis, the output should be structured enough to support affordability rules, not just OCR text.

WPS salary evidence is strong when available. MoHRE says UAE labour market legislation requires private-sector establishments to pay workers monthly through the Wage Protection System, and the 2025 WPS update covered more than 99% of private-sector workers. For BNPL, WPS-linked salary data can reduce reliance on applicant-submitted salary certificates.

Credit reports matter for obligations and exposure. Under the CBUAE short-term credit framework, credit information must be requested before credit is extended at AED 5,000 or more. The credit report does not replace income analysis, but it helps prevent a provider from missing existing credit exposure.

Open finance data is the direction of travel. As API coverage matures, consent-based account data can replace many PDF workflows. Until then, the practical architecture should support both paths: direct account data where available, document-based bank statement analysis where it is not.

Salary certificates and employment letters still have a place, but they should be treated as supporting evidence. They are easy to produce, easy to alter, and often not enough to prove actual cash flow.

Where Fraud and Affordability Risk Enter

The fraud risk in BNPL is usually not dramatic. It is often a small income edit that lets a borrower pass a limit rule.

A salary certificate can be changed from AED 6,500 to AED 16,500. A bank statement can have a bounced payment removed. A cash deposit can be added before application to make the account look healthier. A fake employer letter can be paired with a genuine Emirates ID. These are exactly the cases that visual review misses because the document still looks professional.

The affordability risk is just as important. A borrower can submit genuine documents and still be overextended. BNPL commitments may be spread across different providers. Credit card minimums, personal loans, car finance, remittances, and repeated overdraft behavior may all affect repayment ability.

This is why document fraud detection and transaction analysis belong in the same workflow. Fraud detection answers whether a submitted file can be trusted. Transaction analysis answers whether the borrower can repay.

For BNPL teams, the riskiest cases usually have a mixed signal:

- income appears real, but recurring obligations are high;

- the salary certificate is clean, but salary credits do not match the amount;

- a bank statement is complete, but metadata suggests it was edited;

- the applicant passes KYC, but income is variable and the credit limit is too high;

- the credit amount is small, but the applicant has repeated short-term credit usage.

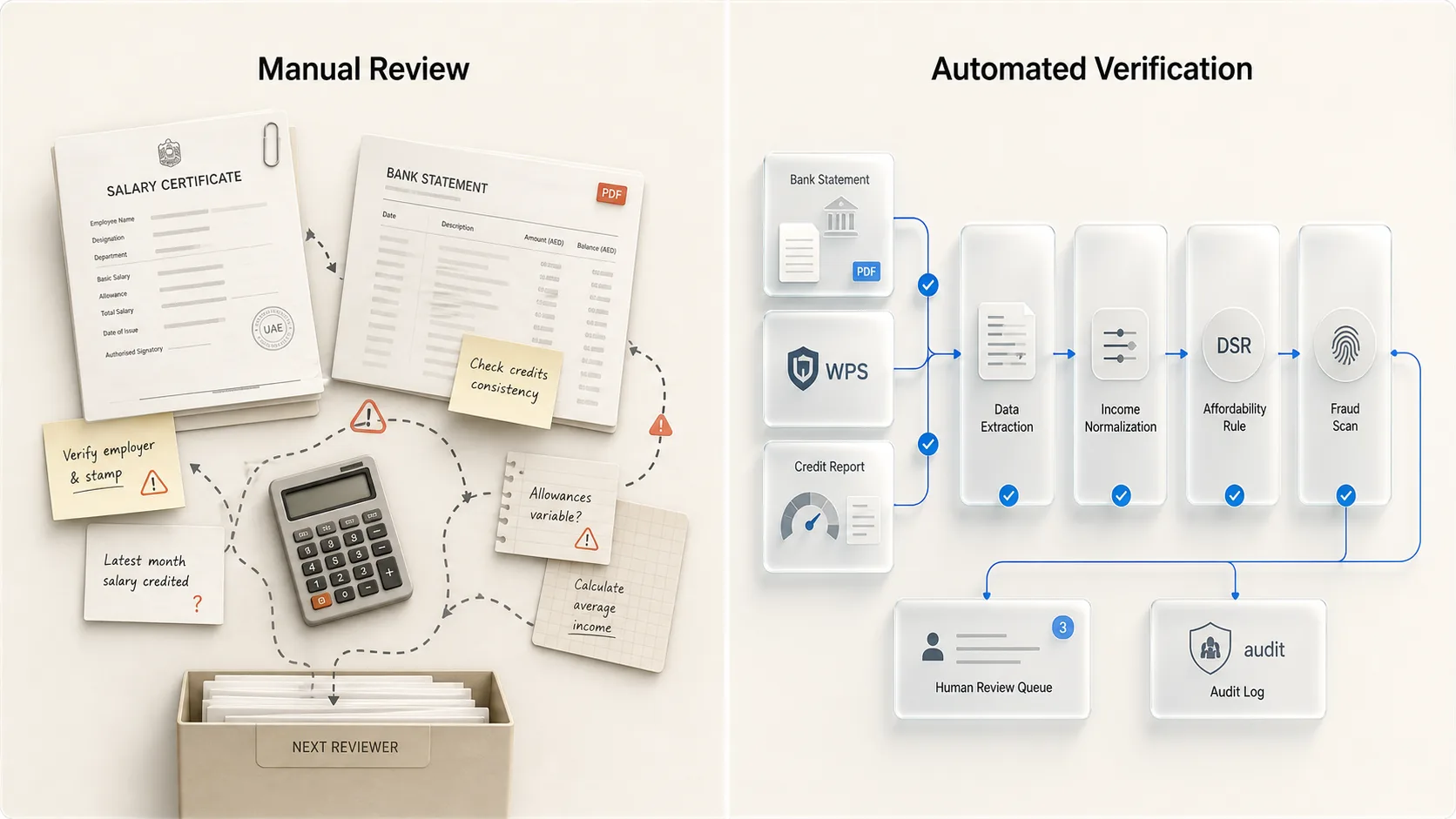

Manual Review vs Automated Verification

The goal is not to remove the compliance officer. The goal is to stop asking the compliance officer to be an OCR engine, fraud model, transaction classifier, spreadsheet calculator, and audit logger at the same time.

| Verification task | Manual salary certificate review | Automated income verification |

|---|---|---|

| Net income confirmation | Reads the certificate and may cross-check the bank statement manually. | Extracts salary credits, employer names, account history, and confidence signals. |

| Affordability check | Depends on reviewer notes and manual calculation. | Applies policy rules to verified income, existing obligations, and credit exposure. |

| Credit report trigger | Relies on the officer knowing when the threshold applies. | Triggers based on credit amount and policy configuration. |

| Document integrity | Visual review only, unless a specialist tool is used. | Runs metadata, layout, font, and pixel-level manipulation checks. |

| Exception handling | Escalations are inconsistent and hard to compare. | Routes high-risk or low-confidence cases to human review with reasons. |

| Audit trail | Case notes, PDFs, and email threads. | Structured JSON record of inputs, checks, rules, overrides, and final decision. |

Automated verification should not auto-approve every case. In a regulated credit workflow, straight-through processing is useful only for clean, low-risk applications. The better design is triage: approve simple cases, reject clear failures, and send ambiguous or high-risk cases to a human with the evidence already organized.

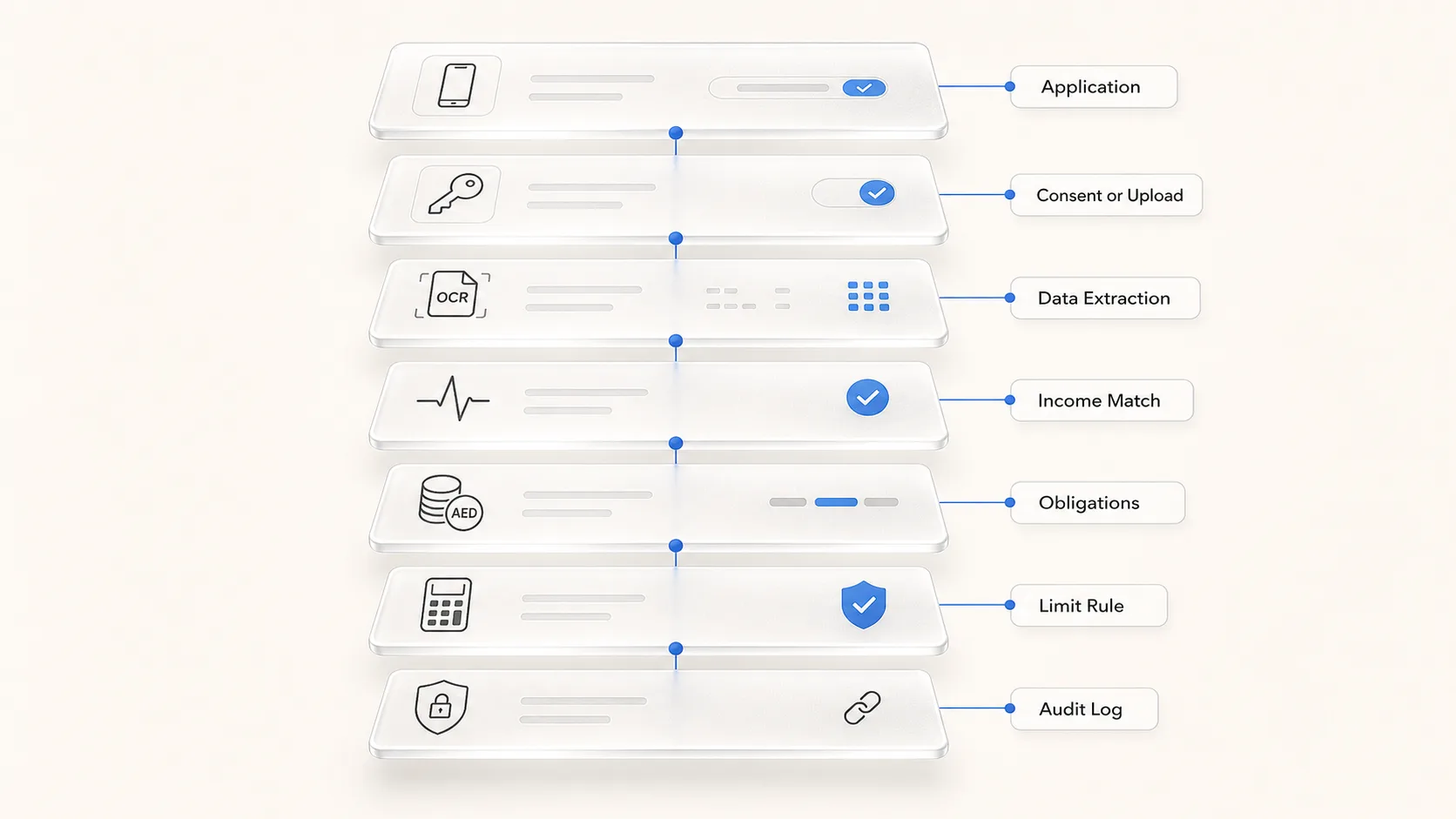

How an Automated Verification Flow Works

A practical BNPL flow starts at application intake. The applicant either consents to account-data access or uploads a bank statement, salary certificate, or both. The system validates file type, identity consistency, and document completeness before any income decision is made.

The next step is extraction. OCR and parsing turn bank statements, salary certificates, and supporting documents into structured data: account holder, IBAN, employer name, salary credits, transaction history, dates, balances, and recurring payment patterns.

Then the system runs fraud and quality checks. Was the PDF edited? Do fonts, metadata, and layout match the expected source? Are there missing pages or altered balances? Does the salary certificate amount align with actual credits? Low-quality or suspicious inputs should not silently pass.

After that, the affordability engine calculates confirmed income, existing debt obligations, recurring BNPL-like payments, liquidity buffers, and the proposed credit exposure. It applies the provider's policy rules and the CBUAE short-term credit constraints.

Finally, the workflow returns a decision package: approved, declined, or needs review. The package should include the verified income figure, confidence score, exposure calculation, fraud flags, credit-report status, rule hits, and reviewer notes if a human override happens.

The output should be machine-readable. A regulator or risk manager should be able to reconstruct the decision without asking the original reviewer what they remember.

Implementation Checklist for 2026

Start with policy mapping. List the checks your BNPL product must perform before credit is granted: identity consistency, verified net income, short-term credit limit, credit-report trigger, affordability assessment, document fraud screening, exception routing, and audit retention.

Then map each policy to data. Do not write "verify income" as a single requirement. Specify the source: WPS salary signal, bank statement salary credits, open finance account data, salary certificate, employer letter, credit report, or a combination.

Build the fallback paths early. Open finance coverage will improve, but not every applicant journey will start with API data. Some applicants will still upload PDFs. Some banks or employment categories will be messier than others. The workflow should be able to degrade gracefully from direct account data to bank statement analysis, and from automated approval to human review.

Keep the review queue small and explainable. A human reviewer should see why a case was routed: document tampering risk, income mismatch, high obligation load, missing credit report, variable income, unsupported bank format, or policy exception.

Measure the system by audit quality, not just speed. Useful metrics include extraction confidence, percentage of cases needing review, false-positive fraud flags, time to decision, income mismatch rate, and number of decisions that can be reconstructed from the audit log without manual explanation.

Finally, connect the article's adjacent controls. BNPL income verification should link to KYC, bank statement analysis, and document fraud detection. Paperwork's KYC automation guide covers identity and onboarding controls, while the bank statement red flags guide shows the transaction patterns lending teams should not miss.

FAQ

Is BNPL regulated by CBUAE in the UAE?

BNPL-style short-term credit is covered by the CBUAE Finance Companies Regulation when offered as a regulated short-term credit activity. Providers should review the rulebook, licensing perimeter, and whether they operate as a finance company, restricted licence finance company, agent, or partner of a licensed bank or finance company.

What is the credit limit for UAE short-term credit?

Under the CBUAE Finance Companies Regulation, the maximum total short-term credit to a borrower is the lower of AED 20,000 or three months of verified net income, subject to any other applicable UAE law restrictions.

Does a BNPL provider need a credit report?

For short-term credit of AED 5,000 or more, the regulation requires credit information to be requested before credit is extended. The provider also needs an affordability assessment and a documented credit file.

Can a salary certificate prove income by itself?

Usually no. A salary certificate can support the file, but bank statement salary credits, WPS salary evidence, open finance data, and credit-report information provide stronger proof of actual income and obligations.

How does open finance change BNPL income verification?

Open finance enables consent-based access to account and product data through standardized API infrastructure. As adoption matures, BNPL providers can use direct account data for income and affordability checks instead of relying only on uploaded PDFs.

Does automation replace the compliance officer?

No. Automation handles extraction, fraud checks, policy rules, routing, and audit logging. Compliance and risk teams still own the policy, exceptions, overrides, and final accountability.

Where should a UAE BNPL platform start?

Start with bank statement analysis and document fraud detection because they cover the widest set of applicants today. Add WPS and open finance integrations as available, then connect the results into one policy engine and one audit trail.

Sources

- CBUAE Finance Companies Regulation, Circular No. 3/2023

- CBUAE short-term credit framework announcement

- CBUAE legislation FAQ for Federal Decree-Law No. 6 of 2025

- Pinsent Masons guide to UAE open finance regulation

- MoHRE Wage Protection System update

- Research and Markets UAE BNPL business report via GlobeNewswire

- Khaleej Times report on the AED 5,000 personal-loan salary threshold

Paperwork's bank statement analysis covers UAE bank formats with DSCR, cash buffer, salary-credit detection, and income categorization built in. Fraud detection runs metadata, font, layout, and pixel-level analysis on every document submission. Try the demo or contact us to discuss your BNPL verification stack.

If you want to learn more, you can try the demo or read our tool documentation.