The best document fraud detection software in 2026 has to catch documents that were never edited at all. Digital forgeries reached 35% of document fraud in 2025, up from a 29% average across 2022 to 2024, according to Entrust's 2026 Identity Fraud Report, and a growing share of those files are generated from scratch: correct fonts, consistent metadata, arithmetic that reconciles. A pixel check finds nothing because nothing was ever pasted over.

This guide compares 12 tools a lending, insurance, property, or compliance team can actually buy. For each one: what it checks, where it is strong, where it falls short, and what it costs when the vendor publishes numbers. Most lists in this category skip the last two. This one treats them as the point.

TL;DR

Paperwork is the strongest pick when the document set is broad or custom: bank statements, salary documents, invoices, contracts, licenses, IDs, application forms, utility bills, and customer-specific templates. It runs all five detection layers, supports custom rules and issuer templates, returns per-check evidence instead of a single score, and deploys as a pay-per-check API or on-premise. Ocrolus Detect is the pick for US lenders that want fraud signals fused with document analytics, and Snappt owns multifamily leasing. Resistant AI is the enterprise forensics engine for banks with an existing intake stack. For identity documents specifically, Regula (on-premise depth) and Sumsub (published pricing, full KYC suite) lead. One caution that applies to every entry: accuracy figures in this market are self-reported, so treat any percentage as marketing until it has run on your own documents.

How we chose

Selection and order follow five criteria, applied the same way to every entry:

- Detection depth: how many independent layers the tool runs (file structure and metadata, fonts and layout, pixel forensics, content cross-checks, issuer and external signals).

- Document scope: financial and business documents, identity documents, or one vertical.

- Evidence in the output: per-check findings a compliance reviewer can defend, versus an unexplained score.

- Deployment: API, dashboard, and whether an on-premise option exists for data-residency requirements.

- Buying friction: published pricing, trials, and whether a mid-size team can start without a six-month enterprise cycle.

Paperwork is our product. It sits first because it is the only entry that pairs all five layers with custom document support, custom rules, pay-per-check API access, and on-premise deployment. It is not limited to one country or one document family; UAE and GCC coverage is a current strength, not the boundary of the product. The criteria above were applied to it unchanged, its limitations section is as blunt as everyone else's, and where a competitor is the better pick, the entry says so. Entries 1 through 8 are document-fraud specialists, 9 through 11 are identity and KYC platforms where document checks are one part of a suite, and 12 is an insurance-claims specialist.

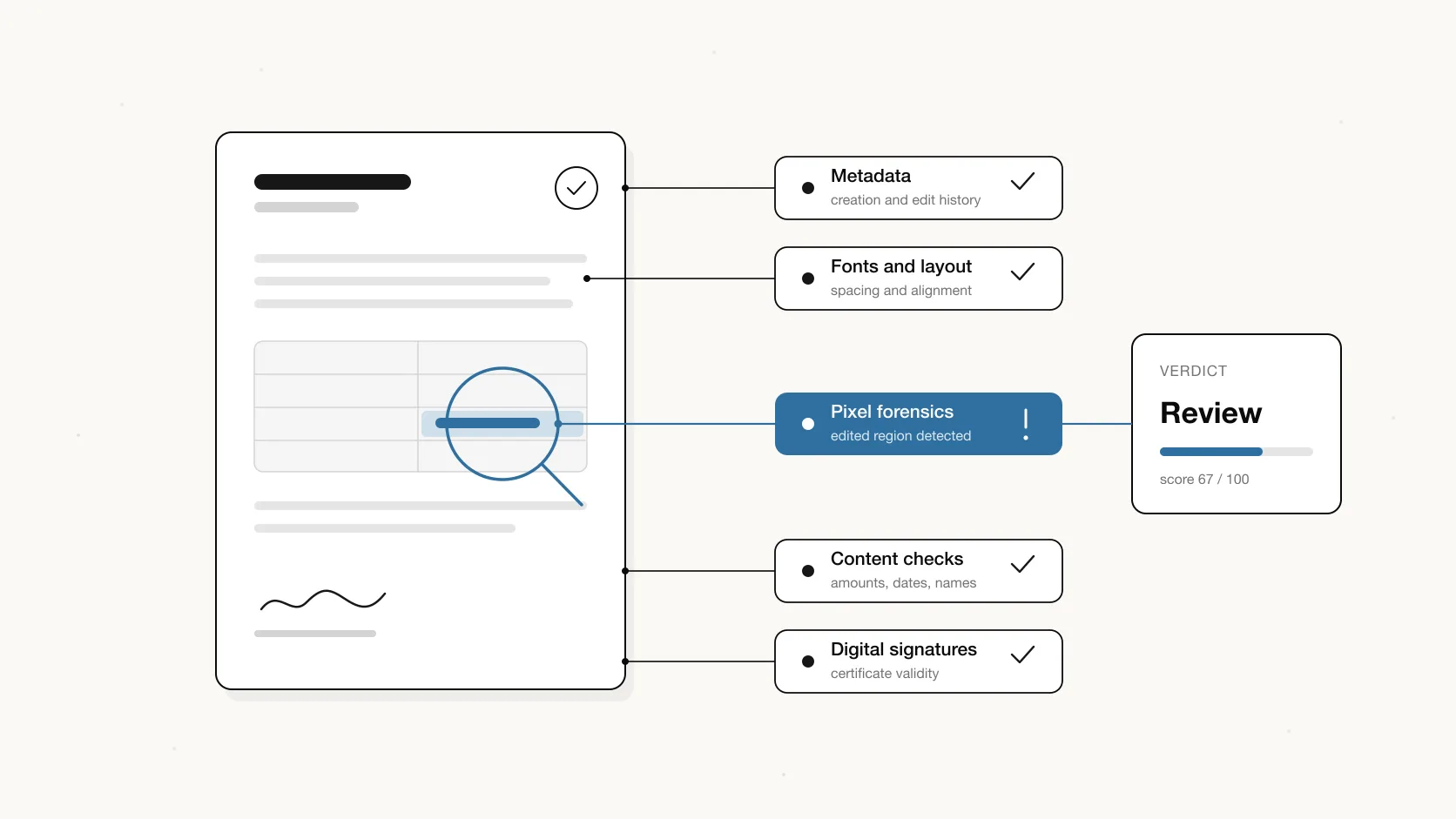

What the five detection layers cover

Every tool on this list works some subset of five layers, and the difference between vendors is mostly which layers they skip. The diagram below shows the five layers and what each one catches.

The first three layers catch editing. The last two catch generation, and generation is where the volume is moving: Signicat's research with Consult Hyperion put 42.5% of fraud attempts against financial institutions in the AI-driven category back in 2024, and Sumsub platform data recorded a 311% year-over-year spike in synthetic identity-document fraud in North America in Q1 2025. The supply side is industrial too: Resistant AI's threat intelligence unit tracked 150+ fake pay stub generators whose top 20 storefronts drew over 10 million visits in 2025, selling stubs for 4 to 35 dollars. For a deeper walkthrough of how each check works, see how document fraud detection works.

The 12 tools at a glance

| Tool | Fraud focus | Best for | Published pricing |

|---|---|---|---|

| Paperwork | Custom financial, business, and identity documents | Global lenders, insurers, platforms, banks | Pay-per-check API; on-premise/custom quoted |

| Resistant AI | Document forensics engine | Enterprise banks and fintechs | From 10,000 USD/month (AWS) |

| Ocrolus Detect | Lending document fraud | US lenders on bank statements | Not published |

| Inscribe | Agentic document review | US banks and credit unions | Not published |

| Snappt | Rental application fraud | Multifamily property managers | Not published |

| Fortiro | Income document fraud | Australian banks and insurers | Not published |

| Finovox | Document fraud analysis | European insurers | Not published |

| Klippa DocHorizon (Doxis AI.dp) | Fraud module inside IDP | EU document processing teams | EUR 25 credit; quote-based |

| Regula | Identity document forensics | Border control, banks, on-premise | Not published |

| Sumsub | KYC suite with doc checks | Regulated onboarding at scale | From 1.35 USD/verification |

| Entrust (Onfido) | Identity verification | Global consumer onboarding | Not published |

| Attestiv | Claims media authenticity | P&C insurers | Free tier; plans quoted |

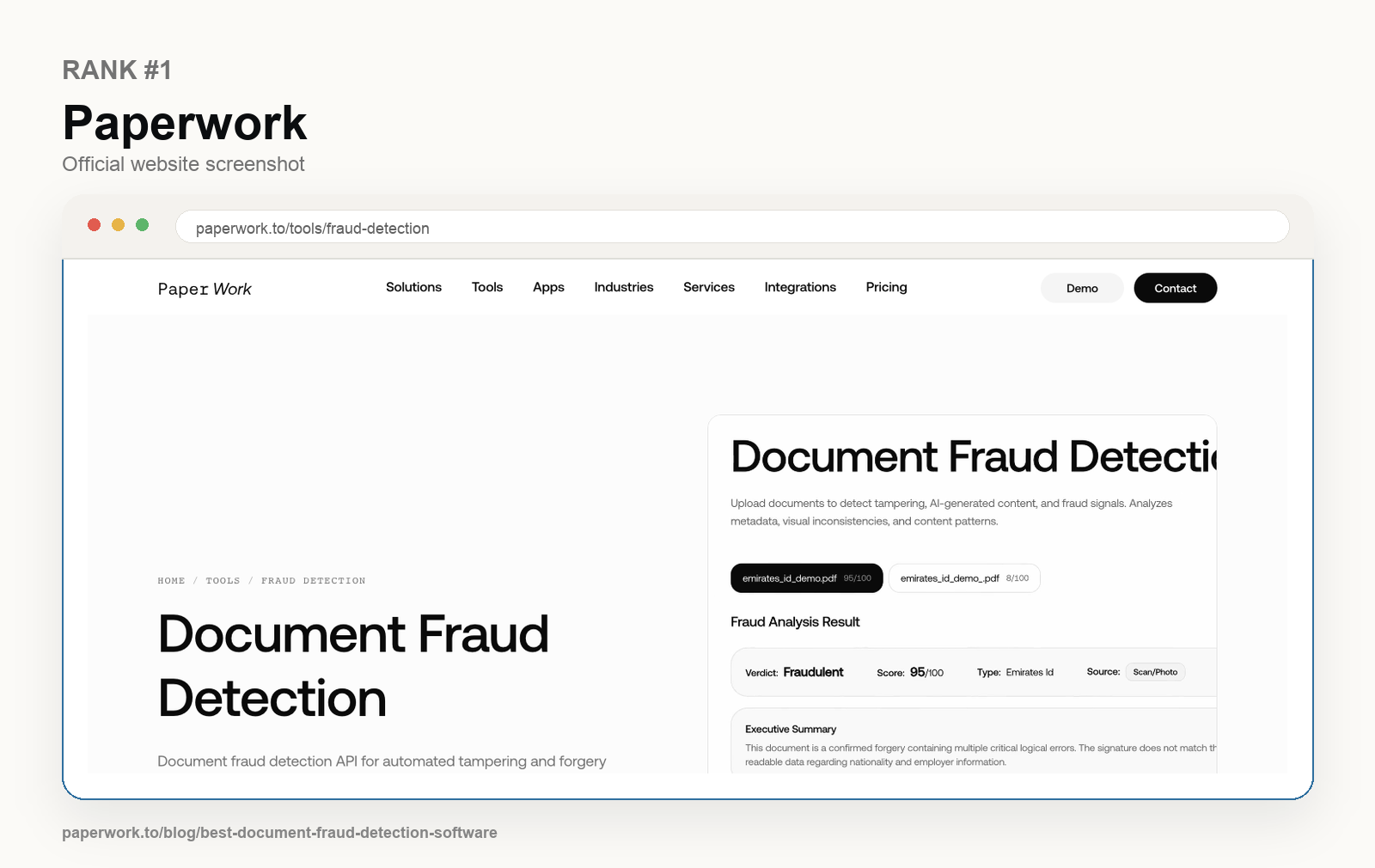

1. Paperwork

Paperwork is a document fraud detection API for custom financial, business, identity, and operational documents. It works best when a team cannot live inside one vendor's narrow document set and needs configurable checks for its own forms, issuer templates, business rules, and review thresholds.

What it does

Paperwork runs all five layers on PDFs, images, and scans: metadata inspection (creation dates, editing software, author trails), pixel-level manipulation checks including error level analysis, font and spacing consistency, layout comparison against known issuer templates, digital signature validation, and content cross-checks that catch amounts, dates, names, entities, and document bundles that do not reconcile. Each check returns its own pass, warning, or fail status with details, alongside an authenticity score, so a reviewer sees why a document was flagged rather than a bare number.

Results arrive in seconds, with batch processing and webhooks for pipeline use. Paperwork covers common financial and business documents (bank statements, pay slips, salary certificates, employment letters, trade licenses, invoices, contracts, IDs, utility bills) and can be configured for custom documents, local issuer templates, house forms, internal policy thresholds, and client-specific fraud checks. UAE and GCC support is strong today, including local banking and business documents, but the product direction is global: the same API pattern applies to US pay stubs, EU invoices, LATAM bank statements, African utility bills, APAC insurance claims, or any custom document a customer needs to verify.

Strengths

- Per-check evidence in JSON output, which shortens compliance reviews, dispute handling, and adverse-action files.

- Custom document support: customers can add issuer templates, field-level checks, business rules, review thresholds, and document-specific fraud indicators instead of waiting for a vendor roadmap.

- Deployment range: pay-per-check API for fast rollout, full on-premise license for banks and regulated enterprises, batch processing, and webhooks for production workflows.

- Regional depth where fraud pressure is high: 66% of UAE businesses reported identity fraud through fake or modified documents in Regula's 2024 survey, but the architecture is not tied to UAE-only documents.

Limitations

- No cross-customer fraud consortium; detection relies on the document itself and issuer templates, not on network history the way Snappt or Inscribe accumulate it.

- Global template coverage depends on onboarding the document families a customer cares about; vertical specialists may have longer out-of-the-box history in niches such as US leasing pay stubs or European ID documents.

- Biometric identity checks (selfie, liveness) are separate tools, not part of the core document fraud API.

Pricing

Pay-per-check API without a mandatory platform fee; custom document setup and on-premise licensing quoted. No public rate card.

2. Resistant AI

Resistant AI is a Prague document forensics engine, founded 2019, that runs 500+ checks per document and is trained on 170 million documents.

What it does

Resistant analyzes how a document was built rather than what it says, which makes it language-agnostic: metadata and editing-tool traces, structural anomalies, template-farm and reused-asset detection across submissions, and detection of the texture patterns image generators leave behind. Verdicts come back as Trusted, Warning, or High Risk with explanations, typically in under 20 seconds. Customers include Payoneer, Dun & Bradstreet, PennyMac, and AXA. The company raised a $25M Series B in October 2025 led by DTCP Growth with Experian and GV participating, and reported reaching breakeven that September.

Strengths

- The widest forensic check set on this list, with published threat research (its pay stub generator study is the reference work on template farms).

- Designed to sit on top of an existing intake or IDP stack rather than replace it.

- Explainable verdicts rather than a bare score.

Limitations

- Enterprise economics: AWS Marketplace lists Document Forgery Analysis at 10,000 USD per month per analysis dimension, which prices out mid-size teams.

- It is a forensics layer, not a document processing suite; extraction and workflow come from elsewhere.

- Thin public review base (three G2 reviews), so reference calls matter.

Pricing

From 10,000 USD/month per dimension on AWS Marketplace; custom contracts otherwise.

3. Ocrolus Detect

Ocrolus Detect is the fraud module of the New York document analytics platform US lenders already use for bank statements and pay stubs.

What it does

Detect combines file forensics (suspicious producer software, anomalous PDF structure, overlapping content, screenshot artifacts) with data-consistency signals that only work because Ocrolus parses the numbers: unreconciled balances, invalid dates, gross pay that does not match, missing Medicare tax on a stub. It visualizes where a document changed and what the field said before. Ocrolus reports finding fraud signals in 6 to 7% of bank statements on its platform, and in a lender test reported by American Banker, it found tampering on over 20% of documents where the lender's manual process had flagged 4%.

Strengths

- Arithmetic-level cross-checks (layer 4) that pure forensics tools cannot run.

- Customer base that doubles as validation: Brex, LendingClub, PayPal, SoFi.

- Tamper visualizations that make chargeback and adverse-action files defensible.

Limitations

- Human-verified processing on complex statements can take hours up to a business day; reviewers on G2 note it is not a seconds-level API for every document class.

- Strongest on US lending documents; thin outside that vertical, and no on-premise option.

Pricing

Not published; sales-led.

4. Inscribe

Inscribe is a San Francisco document fraud platform, founded 2017, that repositioned around AI agents for fraud review while keeping document forensics as the core.

What it does

Inscribe runs four layers: forensic analysis of structure and metadata, comparison against a proprietary database of millions of documents, semantic checks for internal inconsistencies, and perceptual analysis for AI-generation artifacts. Its AI Fraud Analyst packages this as an agent that reviews documents the way a trained analyst would. Its 2026 State of Document Fraud Report found roughly 1 in 16 documents on its network showing signs of fraud, and AI-generated document fraud growing about 5x between April and December 2025.

Strengths

- Network signal from a large proprietary document database, useful against template reuse.

- Agentic review workflow that drafts findings, not just flags.

- Credible research output on AI-generated documents.

Limitations

- Company scale is a procurement question: a 40% staff reduction in March 2024 (TechCrunch), roughly 35 employees, and no funding round announced since the 2023 Series B.

- Financial services only; no on-premise deployment advertised.

Pricing

Not published; demo-led sales.

5. Snappt

Snappt is the dominant document fraud tool in US multifamily leasing, scoring pay stubs and bank statements attached to rental applications.

What it does

Snappt checks submitted documents against formats from 2,000+ financial institutions using models trained on 16 million+ documents, and returns a pass or fail verdict in under 10 minutes. Its 2026 fraud report analyzed 1.46 million applicant submissions in 2025 and found 5.1% carried fraudulently edited documents, with template farms the leading method at 42,600+ cases. The stakes for its buyers are documented: the NMHC fraud survey found 93.3% of multifamily operators experienced application fraud and an average $4.2M written off in fraud-linked bad debt.

Strengths

- Deep issuer-format library for US payroll and banking documents.

- Property-management integrations (Yardi, Entrata, RealPage) and identity verification through a CLEAR partnership.

- Verdicts calibrated for leasing agents, not fraud analysts.

Limitations

- Native digital PDFs only: scans, photos, and screenshots are rejected by design, which pushes paper-based applicants out of the flow.

- Renters have publicly reported legitimate ADP and Gusto stubs failing, with complaints on the company's BBB profile; false positives land on applicants, not staff.

Pricing

Not published; three named tiers, all quote-based.

6. Fortiro

Fortiro is a Melbourne document fraud platform used by Australian banks, non-bank lenders, and life insurers on income documents.

What it does

Fortiro Protect runs 120+ configurable rules plus trained models across content, layout, metadata, and file forensics, adds reverse image search, and detects both classic PDF edits and AI-manipulated images. Unlike Snappt, it accepts photographs and scans, not just native PDFs. Customers include NAB, BOQ Group, AMP Bank, and Pepper Money. In a published Hannover Life Re Australasia case, an 84-document proof of concept flagged 13 documents, confirmed 3 frauds, and projected roughly AUD 450,000 in annual savings.

Strengths

- Input tolerance: PDFs, photos, and scans all processed.

- ISO 27001 certification and a no-retention posture on processed documents.

- Insurance claims coverage in addition to lending.

Limitations

- Geographic concentration: the customer list is Australian, the team is about 20 people, and North America remains an early-adopter program.

- No verifiable product or funding news through 2025 and 2026, so momentum is hard to judge from outside.

Pricing

Not published; sales-led.

7. Finovox

Finovox is a Paris document fraud vendor, founded 2019, serving European insurers and financial institutions.

What it does

Finovox splits the job into four modules: extraction, business-rule validation, fraud analysis (visual forensics, metadata and structure checks, digital-footprint analysis, content checks against external databases), and a case-investigation workspace with evidence reports. Clients include BNP Paribas, MetLife, Swiss Life, and Allianz Direct, across roughly 70 companies in 15 countries. It analyzed about 10 million documents in 2025, reports catching a single EUR 47M fraud that year, and closed an EUR 8.2M Series A in June 2026 led by TX Ventures.

Strengths

- Investigation tooling built for insurance fraud teams, not just an API verdict.

- Fresh funding and tripled 2025 revenue suggest a growing roadmap.

- Coverage of quotes, invoices, and RIB bank details common in European claims.

Limitations

- About 30 employees, so support depth is closer to a startup than to Regula or Entrust.

- Track record is concentrated in Francophone Europe; the UK entry dates to May 2026.

Pricing

Not published; sales-led.

8. Klippa DocHorizon (now Doxis AI.dp)

Klippa DocHorizon is a Dutch intelligent document processing platform with a fraud module, acquired by SER Group in March 2025 and rebranded Doxis AI.dp in March 2026.

What it does

DocHorizon processes 100+ document types and screens them during extraction: EXIF and metadata inspection, copy-move and pixel-level tampering detection, duplicate-submission checks, and cross-checks against third-party databases through its API. Klippa reports customers cutting document fraud by 67% (vendor figure). The fraud checks live inside a no-code workflow builder with 200+ integrations, so intake, extraction, and screening run in one pipeline.

Strengths

- Fraud screening embedded in a working IDP pipeline rather than bolted on.

- EU hosting and GDPR posture for European processors.

- Wide document scope: invoices, receipts, IDs, loyalty submissions, tenant files.

Limitations

- Two brand changes in twelve months (Klippa to SER Group to Doxis AI.dp) make roadmap continuity harder to judge.

- G2 reviewers note accuracy drops on unusual layouts, SLA sold separately, and template work on edge cases.

- Fraud detection is a module of an IDP product, not the core product.

Pricing

Not published per document. One-time EUR 25 platform credit, then pay-as-you-go with quote-based rates.

9. Regula

Regula is a Latvian identity-document forensics vendor, founded 1992, whose SDK checks IDs against the market's largest template library: 16,000+ templates from 254 countries and territories.

What it does

Regula verifies identity documents the way a border lab would: template matching, MRZ and barcode validation, hologram and dynamic print checks, NFC chip reading with server-side reprocessing, and document liveness that catches screens, photocopies, and photo-of-photo submissions. It also builds the physical forensic devices used by border authorities in 80+ countries, and 350+ banks run its software.

Strengths

- Unmatched identity-document template depth and 30+ years of forensic lab lineage.

- Full on-premise and offline capability, the strongest data-residency story on this list.

- Active 2026 roadmap: mobile driver's license reading in January, server-side mDL verification in May.

Limitations

- Identity documents only; invoices, bank statements, and business paperwork are out of scope.

- No public SOC 2 report as of April 2025 (available under NDA), and fast-SLA support is reserved for enterprise contracts.

Pricing

Not published; usage-based custom licensing.

10. Sumsub

Sumsub is a London verification platform covering KYC, KYB, AML screening, and transaction monitoring in one API, used by 4,000+ clients.

What it does

Sumsub verifies 14,000+ identity document types from 220+ countries, runs liveness and face matching, and screens against sanctions and PEP lists. In May 2026 it shipped an Adaptive Deepfake Detector that retrains continuously against new attack types. Its Identity Fraud Report 2025-2026 found sophisticated multi-step fraud up 180% year over year, which is the environment its layered checks are built for.

Strengths

- One contract covers identity, AML, and fraud monitoring; fewer vendors for a compliance team to manage.

- Emerging-market document coverage, including handwritten and rare-script documents.

- Published pricing and a 14-day trial with 50 free checks, which is rare transparency in this market.

Limitations

- G2 reviewers report sanctions-screening false positives pushing legitimate users into manual review.

- Identity onboarding focus: bank statements, invoices, and business documents are outside its fraud scope.

Pricing

Published: 1.35 USD per verification with a 149 USD monthly minimum; the Compliance plan is 1.85 USD per verification with a 299 USD minimum.

11. Entrust (formerly Onfido)

Entrust identity verification, built on the Onfido platform acquired for $650M in April 2024, verifies 2,500+ identity document types across 195 countries.

What it does

The Atlas AI engine runs 10,000+ micro-models against specific fraud vectors: template and security-feature checks, image forensics on IDs, selfie and video liveness, deepfake and mask detection, and injection-attack detection. Entrust's own 2026 report data shows why the biometric side matters: deepfakes appeared in one of every five biometric fraud attempts, and deepfake selfies rose 58% in 2025.

Strengths

- Country coverage and throughput built for consumer onboarding at bank scale.

- Fraud intelligence fed by a dedicated lab and known-fraud document data.

- Part of a wider identity-security portfolio, which consolidates vendors for large enterprises.

Limitations

- G2 and Trustpilot reviewers report genuine documents rejected over framing or appearance changes, and flag diagnosis that takes digging.

- Quote-based enterprise pricing with no low-commitment tier, and identity documents only.

Pricing

Not published; quote-based.

12. Attestiv

Attestiv is a US media and document authenticity platform for insurance, founded 2018, that scores photos, videos, and documents with a 1-to-100 tamper score.

What it does

Attestiv detects Photoshop edits, splicing, AI-generated images, and screen recaptures in claim photos, and scores documents on text-modification probability, PDF metadata tampering, and arithmetic consistency. A February 2026 ReSource Pro partnership embedded it into insurer workflows.

Strengths

- Claims-triage focus: adjusters get one tamper score per artifact, in seconds.

- Free tier (5 scans per month) makes evaluation trivial.

- Deepfake video analysis that combines metadata with transcript context.

Limitations

- Accuracy claims (97% ROC AUC minimum) are vendor-stated, with almost no third-party review footprint to check against.

- Insurance and media centric; not built for lending-grade bank statement or identity template verification.

Pricing

Free tier with 5 scans per month; business plans quoted.

Also considered

Several tools show up in this category without being document-fraud software in the strict sense. Sensity AI is the strongest dedicated deepfake detector (900,000+ incidents identified in 2025, by its own count) but its current product is synthetic-media-first, with static document forensics secondary. Jumio, ComplyCube, and Socure are identity and KYC platforms in the same bracket as Sumsub and Entrust. Mitek covers cheque fraud and added deepfake and injection detection in February 2026. Nanonets is document processing with anomaly flags, not fraud-first, by its own positioning. Koncile pairs invoice-focused extraction with fraud checks. In the merchant-cash-advance niche, Heron Data, ClearStaq, and MoneyThumb compete on bank-statement checks for brokers. LexisNexis FraudNet and Middesk solve adjacent problems (identity networks, business verification) without document-level tamper analysis.

How to choose for your use case

The market is consolidating fast (MarketsandMarkets sizes fraud detection and prevention at $32B in 2025, heading to $65.68B by 2030), but the practical decision still comes down to which documents you accept and where they come from:

- US consumer or SMB lender on bank statements and pay stubs: Ocrolus Detect if you want analytics and fraud in one platform, Inscribe if you want agentic review with a network signal.

- Multifamily property manager: Snappt for native-PDF applicant flows; if your applicants submit scans and photos, test input tolerance before contracting.

- European insurer: Finovox for claims investigation workflows, Resistant AI for a forensics engine under an existing stack.

- Australian bank or life insurer: Fortiro.

- Global consumer onboarding where the ID is the document: Sumsub for published pricing and a bundled suite, Entrust for enterprise scale, Regula when everything must run on-premise.

- Global lender, insurer, bank, or platform with a mixed or custom document set: Paperwork, especially when the workflow needs custom templates, custom rules, evidence JSON, API integration, and on-premise deployment. UAE and GCC templates are a strength today, not the limit of the product.

- Insurance claims with photo evidence: Attestiv, or Fortiro where claims include income documents.

Whatever the vertical, the spend math is not subtle. Alloy's 2026 State of Fraud report found 67% of banks, credit unions, and fintechs saw fraud rise in 2025 and 22% lost more than $5M to it, while the ACFE's Occupational Fraud 2026 report puts the median single fraud case at $104,000. A document check that costs cents per file prices against numbers like these.

Frequently asked questions

What is document fraud detection software?

Document fraud detection software analyzes submitted files (PDFs, scans, photos) for signs of tampering or fabrication: metadata inconsistencies, edited pixels, mismatched fonts, cloned regions, arithmetic that does not reconcile, and layouts that deviate from the issuer's real template. It returns a verdict with evidence so a reviewer can act on it. It is distinct from identity verification, which ties a person to an ID; document fraud tools examine any document that carries money-relevant data.

Can software detect AI-generated fake documents?

Yes, but not with pixel forensics alone. A generated document has no edit history, so detection shifts to layers a generator cannot fake cheaply: semantic cross-checks (does the pay math reconcile, do dates and balances line up across pages) and issuer verification (does the layout match how the real bank formats statements). This matters at current growth rates: Inscribe measured AI-generated document fraud growing about 5x over nine months of 2025, and Entrust's 2025 report recorded a deepfake attempt every five minutes during 2024.

How much does document fraud detection software cost?

Most vendors quote per document or per verification and do not publish rates. The published reference points: Sumsub starts at 1.35 USD per verification with a 149 USD monthly minimum, Resistant AI lists from 10,000 USD per month per analysis dimension on AWS Marketplace, Attestiv has a free tier of 5 scans per month, and Paperwork prices per check through its API with custom setup quoted for new document families. Enterprise document forensics contracts are typically annual and volume-based.

Do I need document fraud detection if I already run KYC?

Yes, if you accept any document beyond the ID. KYC verifies who the person is; it does not check whether the bank statement, salary certificate, or invoice that person uploads is genuine. Lending fraud lives in exactly that gap, which is why bank statement red flags deserve their own review step, and why lenders increasingly run a document verification API across the whole application file rather than the ID alone.

How accurate is document fraud detection software?

Every accuracy figure in this market is self-reported: Snappt claims 99.8%, Resistant AI publishes 99.2% on its site and 99.92% on its AWS listing, Ocrolus states a 90%+ true positive rate. No independent benchmark exists across vendors. The practical test is a proof of concept on your own recent documents, including a handful of known frauds, measured on both catch rate and false positives, since a false positive lands on a real customer.

Can document fraud checks run on mobile submissions?

Yes, if the tool accepts photos and scans rather than only native PDFs; Snappt, for example, rejects photographed documents by design, while Fortiro and Paperwork process them. For mobile-first onboarding, the Paperwork app captures documents, reads passports via NFC, and feeds the same verification pipeline.

Where Paperwork fits

Paperwork's fraud detection runs the five layers this article used as its yardstick, returns per-check evidence in JSON, and ships as a pay-per-check API or an on-premise deployment. It is built for teams whose real intake is messy: global document sets, local issuer formats, custom templates, custom business rules, scanned files, images, PDFs, and multi-document application bundles.

It sits alongside bank statement analysis, KYC extraction, and business verification in one platform, so a lending or compliance team can screen the whole application file, not just the ID. Try it on a sample document.

If you want to learn more, you can try the demo or read our tool documentation.